If you have children or grandchildren born between January 1, 2025, and December 31, 2028, you have probably seen the headlines about Trump Accounts for children.

The basic story sounds simple enough: eligible children may receive a one-time $1,000 federal contribution, the money can be invested, and over many decades the account could grow into something meaningful by retirement.

Most of the excitement is not misplaced. Starting early matters. Compound growth is powerful. A small amount of money invested for a very long time can become much larger, much like planting an oak tree when everyone else is still shopping for shade.

However, as is often the case with financial headlines, the fine print matters more than the headline.

Before parents or grandparents rush to open a Trump Account, there are a few important details worth understanding.

What Is a Trump Account?

A Trump Account is a new type of retirement account for children. It is designed to help create an early savings foundation, with the account established for the benefit of the child.

For eligible children born between January 1, 2025, and December 31, 2028, the federal government may make a one-time $1,000 contribution to the account. Families may also be able to add additional contributions, subject to the rules and limits applicable to these accounts.

At first glance, this may sound like a college savings account. It is not.

A Trump Account is closer to a retirement account than a 529 plan. That distinction matters.

Is a 529 College Savings Plan better?

One of the biggest misunderstandings about Trump Accounts for children is the belief they are primarily designed for college.

They are not.

A 529 plan is usually still the better tool when the primary goal is education funding. A properly used 529 plan allows money to grow tax-deferred and come out tax-free when used for qualified education expenses. It also gives families more direct alignment between the account and the goal: paying for school.

A Trump Account, by contrast, is a long-term retirement-oriented account. During the child’s early years, access to the money is restricted. Once the child reaches the applicable age, the account generally begins to follow rules similar to a traditional IRA.

That means withdrawals may create income tax, and early withdrawals for the wrong purpose may also create a 10% penalty.

In plain English, if the family’s goal is college, the Trump Account is probably not the first tool to reach for. It may still have value, but it should not automatically replace a 529 plan.

Trump Account vs. 529 Plan: Which Is Better?

The better question is not whether a Trump Account is “good” or “bad.” The better question is what job the account is being asked to perform.

A 529 plan is generally built for education.

A Trump Account is generally built for long-term retirement savings.

Those are different tools for different purposes. A hammer and a golf club both involve swinging something, but only one belongs on the first tee.

For families trying to decide between a Trump Account and a 529 plan, the planning question should be simple:

What is the money for?

If the goal is college, private school, trade school, or other qualified education expenses, a 529 plan may still be the more effective choice.

If the goal is to begin building a long-term retirement foundation for a child, especially with the benefit of the one-time federal contribution, a Trump Account may be worth considering.

For many families, the answer may not be either/or. It may be both, but in the right order and with the right expectations.

Who Can Open a Trump Account for a Child?

This is one of the most important details for grandparents.

The rules governing who may open a Trump Account are not as casual as the headlines make them sound. The IRS rules create a specific framework for who may act on behalf of the child, and the rules may differ depending on whether the person is simply opening the account or also requesting the $1,000 federal contribution.

In general, a child’s legal guardian or parent will usually be the first person to consider. In some circumstances, an adult sibling or grandparent may be able to act, but grandparents should be careful before assuming they have authority to open the account.

This is especially important because a form may allow someone to sign, but the form does not always stop a person from signing incorrectly.

That is how many tax mistakes happen. The paperwork accepts the ink, but the rules may not accept the conclusion.

For grandparents who want to help, the safer approach is usually to coordinate with the child’s parent or legal guardian before opening anything.

Should Grandparents Open Trump Accounts?

Grandparents may be excited about Trump Accounts because these accounts feel like an easy way to help grandchildren get a financial head start.

That instinct is a good one. The execution needs care.

Before opening a Trump Account for a grandchild, grandparents should ask:

- Does the child already have a Trump Account?

- Is the child eligible for the $1,000 federal contribution?

- Who has legal authority to open the account?

- Are the parents already using a 529 plan?

- Would additional savings be better directed to education, retirement, or another family priority?

- How does this fit into the family’s broader estate, tax, and gifting plan?

The goal is not merely to open another account. The goal is to put the right money in the right vehicle for the right reason.

When a Trump Account May Make Sense

A Trump Account may be worth considering when a child is eligible for the $1,000 federal contribution and the family wants to begin building long-term savings.

It may also make sense when parents or grandparents already have education funding under control and want to create an additional long-term account for the child’s future.

The key is understanding the purpose. This is not simply “free money.” It is free money inside a specific type of account with specific rules.

Used correctly, it may be a helpful planning tool. Used carelessly, it may create confusion, tax friction, or unrealistic expectations.

Coordinate the Plan

Financial tools work best when they are coordinated. A Trump Account should not be viewed in isolation from the family’s 529 plan, estate plan, gifting strategy, or broader tax picture.

For some families, the Trump Account may be a useful addition.

For others, the 529 plan may remain the priority.

For grandparents, the best first step may be a family conversation before taking action. Not every good idea should be implemented in the first five minutes. Sometimes the better planning answer is to slow down just long enough to avoid stepping on the rake.

Final Thought

Trump Accounts for children may become a meaningful planning opportunity, especially for families with children or grandchildren born between January 1, 2025, and December 31, 2028.

However, they should be understood for what they are: retirement-oriented accounts for children, not college savings accounts.

Before opening a Trump Account, make sure you understand who has authority to open it, whether the child qualifies for the $1,000 federal contribution, and how the account fits alongside any existing 529 plan.

This is not a complicated conversation, but it is one worth having before the paperwork is filed.

At Almega Wealth Management, we help families think through these decisions in the context of their broader financial, tax, and family wealth plan. If you are considering a Trump Account for a child or grandchild, we can help you determine whether it fits, who should open it, and how it coordinates with the planning already in place. To schedule an exploratory call with us, please click here.

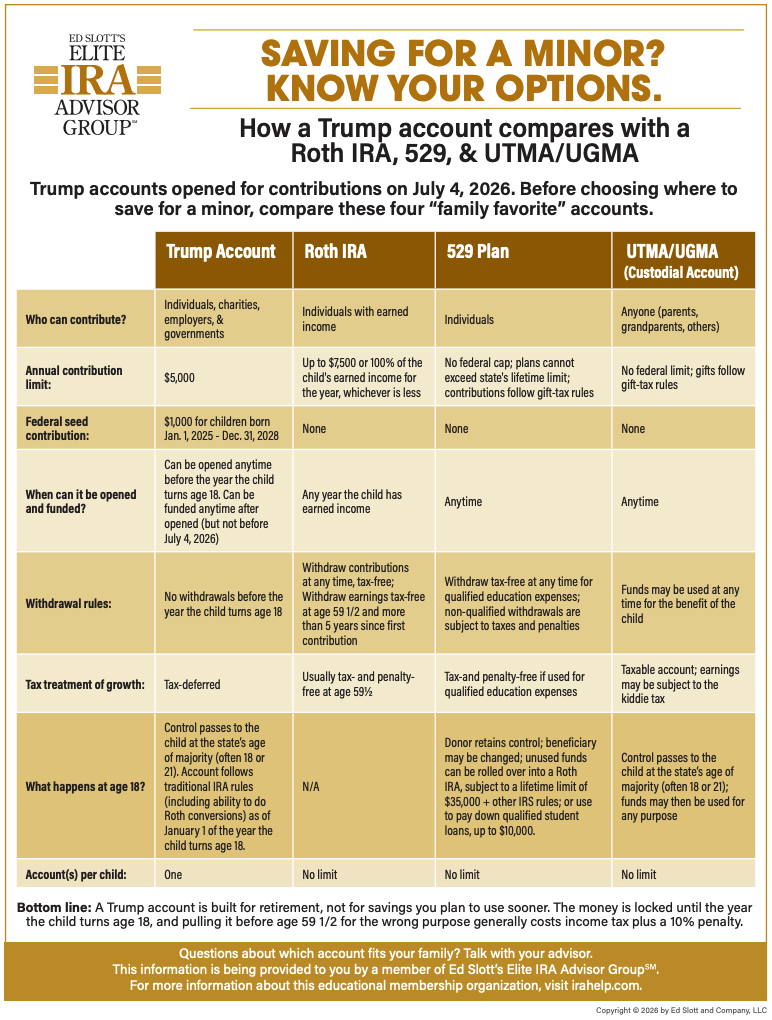

Download a Comparison Chart

As a member of Ed Slott’s Elite IRA Advisor Group, we have made available for you to download a copy of the comparison chart developed by Ed Slott.

Disclosure: This article is for general educational purposes only and should not be treated as individualized tax, legal, or investment advice. Before opening or funding any account, consult your financial advisor, tax professional, or legal advisor.